Vacations, new cars, fancy hotels, eating out! We all dream about such lavish desires at one point or another in life. We all love vacations. I like traveling and I always fancied traveling for a vacation. When I thought of vacations, I used to think of flying in airplanes, staying at hotels, eating out, going out for sightseeing, walking the beach etc. Planes, hotels, and eating out are a big part of travel experience and they are also a major part of your vacation budget.

I travel for my job

I travel for my job for few months in a year. During that time, I stay in hotels, fly on the airplane, drive rental cars. I also eat out every day. I also make some time to visit nearby attractions, meet friends that are in the area, and occasionally invite Mrs. Millionare Immigrant (MI) for a vacation and enjoy the off days with her. What a dream job, right? Yes and no, I do like my job and like the fact that I get a bigger paycheck when I travel. I also save on the cost of food and gas as all my expenses are paid for by my employer. But staying at a hotel, eating out every day, and driving fancy rental cars is not that fun after you do it for a while.

Hotels are not that special

We all look at fancy hotel rooms and say wow! During our vacations, Mrs. MI always makes sure to take pictures of the “beautiful” hotel room before I “make a mess”. But, after living in hotels for months, you realize that there is really nothing special about hotel rooms. It is not any different from your apartment or house. You get the cleaning staff and new towels every day, but that is not that exciting after weeks or months.

I also get free breakfast at the hotel and sometimes free drinks and snacks in the evening, and they also lose their charm after a while.

Flying on the airplane must be fun

Flying on an airplane is a nice adventure if you do not fly as much. You may love the experience if you were flying for a vacation. I still enjoy it most of the times. I like how in a matter of hours, you can get to an entirely different part of the country/world.

I also like the view from the sky. I always feel so powerful looking down on the land below. I especially like to look at houses and see how ‘tiny’ they look. It amazes me that people have to struggle all their life to own/pay for a ‘tiny’ house on a ‘tiny’ land, which looks really tiny from up there. I always think that all I need to do is to own a bunch of those ‘tiny’ houses and I will be set for life. It looks so doable and I feel motivated.

Back on the subject, I don’t mind flying once every week, which is what I do mostly when I travel for work. On longer flights and in long transits, I sometimes get impatient, but it is not that bad when you know you are getting paid for all of that.

What about food?

Food and drinks are a big part of travel and vacations. Some people travel just for food. I also enjoy eating and trying new food and travel allows you to do that. Eating out every day, twice a day, allows you to play with your test buds and explore the local restaurants to the fullest.

But like everything else, it is only fun for a while. After few weeks, it is not that fun. I almost got sick eating out on one of my first trips for work. I was having a lot of fun eating at local restaurants with my coworkers and after about a week, I did not feel like eating anything. I remember coming back home to Mrs. MI’s lovely home-cooked dinner, and I could not eat anything at all. It took a few days of the home-cooked meal before I gained my appetite back.

You will pretty soon realize that nothing can beat a good home-cooked meal. After eating the greasy breakfast for weeks, your oats and banana breakfast tastes so good. No matter how much you try to diversify your food choices, you start craving for simple home cooked lunch and dinner.

Ok, I get that. But rental cars are fun, right?

Picking up a car of your choice from the car rental aisle sounds so much fun. I have to agree that this is still fun even after years, especially if you have the elite membership. At home, I drive a used car that is 15 years old, so any rental car is an upgrade. But I always like to pick cars that I have not driven before. In the past, I always went for Sports cars. But since I realized the number of blind-spots they have, I rarely pick them these days. I also have some favorites, which are mostly based on how comfortable seating and driving is on those vehicles.

Although I enjoy driving them, I soon realized that even the fancier cars are not that different from a simple car. Yes, they are an upgrade but all they do is take you from point A to point B just like your simple used car. The difference in price between an older economic car and a fancy new car is too much compared to the difference in your driving experience.

Yes, the rental car aisles do not provide the fanciest cars. But I feel that I can extrapolate the results.

The result: I no longer desire for new cars or fancy restaurant food

I am sure you can tell by now that I lost my desires for fancy new cars, restaurant food or staying at a fancy hotel.

I was not always the same. I used to dream of driving a nice car. Before I bought my current car, I was planning on buying a truck or a sports car (thank goodness!).When we had just one car in our family, I was planning on buying a brand new second car. But when the time came, we actually bought an even older used car. Thanks to my travel that I got rid of my expensive hobby.

I am so satisfied that my car does the same job a nicer car would do.

We have also cut down on eating out so much. We still eat out occasionally, mostly when we do not feel like cooking or just to get a break. Our choices are also less expensive. Eating out a lot makes you realize that pricier food does not mean it tastes better.

My vacation choices have changed

I also realized that what you enjoy on a vacation is not the fancy hotels, fancy restaurants or even the fancy beaches. It is who you are with that you enjoy the most. Beaches from Miami to Santa Monica all look the same on a warm day.

I still go on vacations, probably more than in the past. But my vacations are more focused on being close to nature, meeting friends and family, meeting the local people and knowing their culture. I think my vacation choices are more meaningful and satisfying these days.

In the meantime, I have also saved a lot by getting rid of a number of my expensive desires. Thanks to my work travel.

What about you?

How often do you travel? Has your travel choices and other life choices changed because of your travel experience?

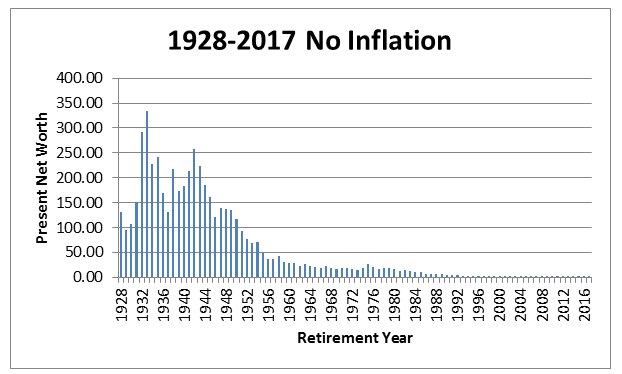

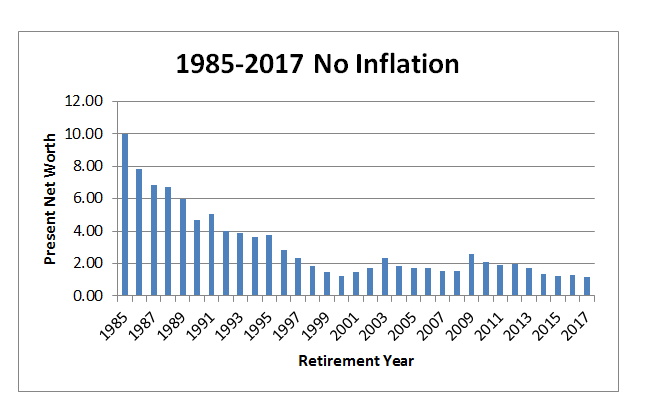

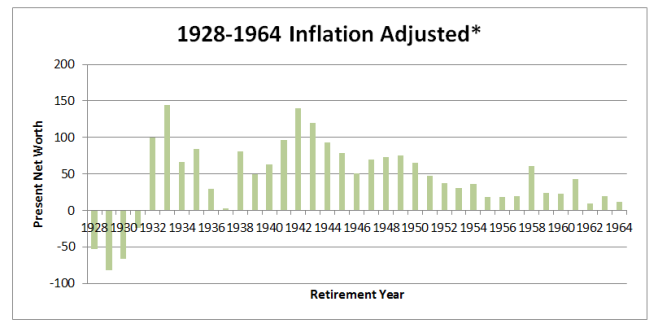

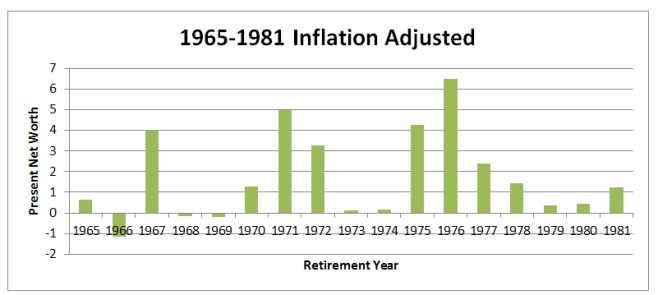

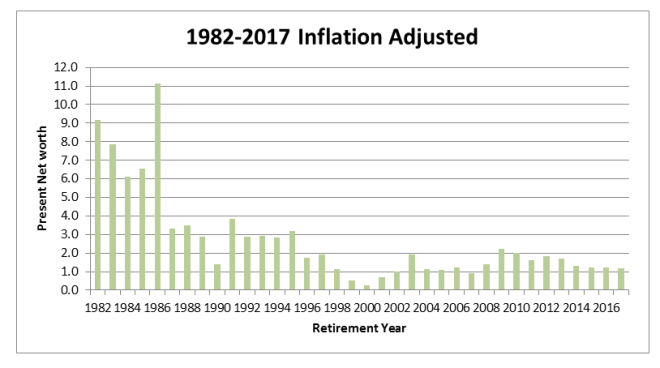

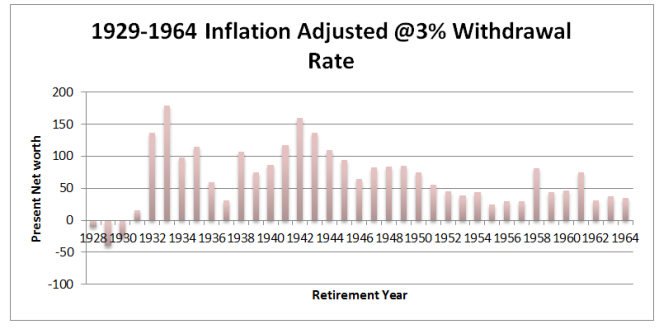

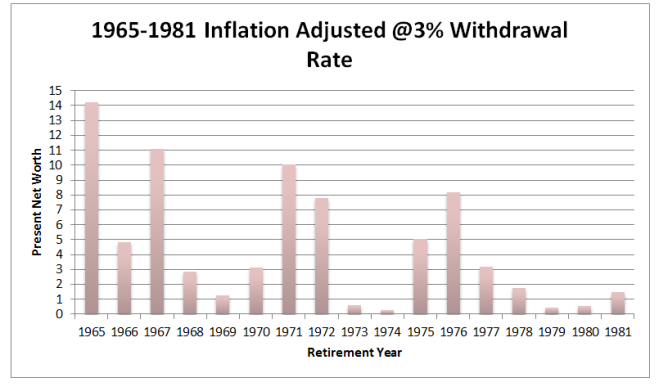

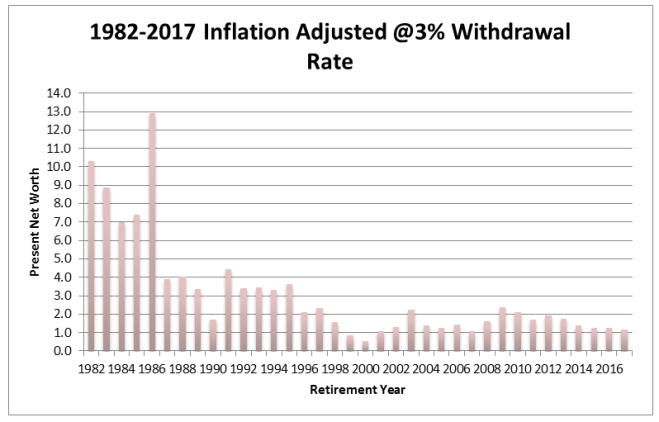

I have written before about 4% withdrawal rate. It is a considered to be a safe withdrawal rate for retirees. However, I admit that it is not perfect.

I have written before about 4% withdrawal rate. It is a considered to be a safe withdrawal rate for retirees. However, I admit that it is not perfect.